Emerging markets are about to leapfrog fossil fuels to generate all the growth in their electricity supply from renewables in this decade. The peak global fossil fuel usage for electricity generation was probably 2018. The emerging markets are key to the global transition.

The study ‘Reach for the sun: The emerging market electricity leapfrog’ by Carbon Tracker Initiative and the Council on Energy, Environment and Water (CEEW) provides an overview of the emerging market electricity leapfrog. It demonstrates that emerging markets will not follow the same path to renewables as the developed markets.

The study discusses how the developing countries are about to leapfrog fossil fuels in this decade to generate all the growth in their electricity supply from renewables. It focuses on types of leapfrog, the different groups of emerging markets, how advanced the leapfrog is, the forces driving the leapfrog as well as the various barriers to change.

Key findings

About 88 per cent of the growth in electricity demand between 2019 and 2040 is expected to come from the emerging markets. If they do not leapfrog to renewables, there will be no global energy transition.

Leapfrog means growth. Whilst a total transition is hard, the leapfrog is more achievable because it requires emerging markets to generate the increase in their domestic demand from renewable electricity, improving energy security.

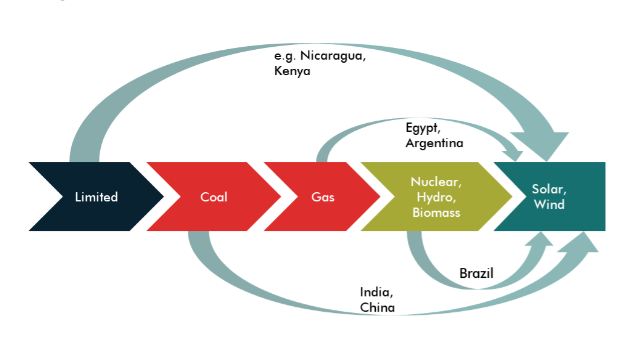

There are four key groups of emerging markets. These are: China, which is nearly half the electricity demand, and 39% of the expected growth; other importers of coal and gas such as India or Vietnam, which are a third of the demand and nearly half the growth; coal and gas exporters such as Russia or Indonesia, which are 16% of demand but only around 10% of the growth; and ‘fragile’ states such as Nigeria or Iraq which are 3% of demand and around the same share of growth.

Many countries have already leapfrogged. Developed market demand for fossil fuels for electricity generation peaked in 2007, and is down 20% since then; 99% of developed markets have already seen a peak. Meanwhile, South African fossil fuel demand for electricity peaked in 2007, Chile in 2013, Thailand in 2015, Turkey in 2017.

India’s double leapfrog — connecting nearly all households to electricity and its renewable energy rollout — is one of the most revolutionary in scale. While its fossil fuel demand for electricity has plateaued for now, it could rise again as the economy recovers unless energy storage prices fall rapidly.

Emerging markets except China have reached a peak. In emerging markets ex-China, fossil fuel demand for electricity has already peaked in countries with 63% of total demand. Even in 2019, 87% of the growth in electricity supply came from non-fossil sources. China is likely to peak before 2025.

China is also on the cusp of change. Chinese electricity demand per capita is about the same as in Europe, and in 2020 two-thirds of the growth in supply came from non-fossil sources. Solar and wind are already at 10% of generation, and growing capacity at over 20% a year.

Domestic drivers of change are very powerful. Renewables are the cheapest source of new electricity in 90% of the world, and the rest will soon follow. Emerging markets have massive renewable flows, 140 times greater than their energy demand. The move to renewables will save millions of lives lost to fossil fuel pollutants, reduce energy dependency for the 80% of people living in fossil fuel importer countries and drive local job creation.

Global drivers can speed up the shift. Meanwhile, leaders of the countries with over 70% of global GDP have pledged to get to net-zero by mid-century, competition between China and the US favours a rapid dissemination of renewable technologies, and capital markets are increasing the cost of fossil capital relative to renewables capital. Expect more global technical, financial and policy support, a key prerequisite of a successful COP26.

The barriers to change are all soluble. Intermittency can be managed; solar and wind are still only 4% of emerging market ex-China electricity supply, far below the current feasibility ceiling. With the right policies, system costs are lower than those of fossil fuels.

The capital requirements of new renewable based electricity systems are not necessarily higher than those of fossil fuels. Systemic barriers exist, but apply to all energy sources.

The solution of choice for access. For many electricity-deprived people, domestic renewables provide a superior new solution to drive energy access and power livelihoods. For example, 84% of the expected provision of electricity access in the IEA net zero forecast is from renewables. There is an opportunity for a double leapfrog — from no electricity to access to clean, reliable and affordable electricity for all.

Domestic policy is key. Change is nevertheless hard, and needs policy to liberalise markets, introduce auctions and attract capital. Climatescope analysis shows that countries with appropriate policies in place have attracted 16.5 times as much capital as those without.

Vested interests are holding back change. In some coal and gas exporters and fragile states, vested interests are still able to manipulate the political process to hold back change. But these laggards are too small to stop the global shift.

How the balance of forces will play out. 82% of demand comes from coal and gas importers where the balance of forces favours a leapfrog. 16% of demand comes from coal and gas exporters, some of which like South Africa are already changing. 3% of demand comes from fragile states, which are likely to need considerable external support.

How to speed up the leapfrog. Developed market policymakers need to identify those countries where the political economy favours a leapfrog, transfer policy and technology expertise and help reduce the cost of capital.

There is a moral case for access. About 770 million people still lack access to electricity. They constitute a small share of forecast growth in electricity demand until 2040. But the international community has a moral obligation to support universal electricity access as the basis for achieving many other sustainable development goals.

There is critical need for financial support to drive down prices of storage technologies and cover for current gaps between renewables-plus-storage versus coal. Without such support, either the pace of the energy transition would be slower or many energy-poor people would be trapped at low levels of energy consumption. Neither is morally acceptable.

The full report can be accessed here

Suggested citation: Bond, Kingsmill, Arunabha Ghosh, Ed Vaughan, and Harry Benham. 2021. Reach for the sun: The emerging market electricity leapfrog. A Carbon Tracker-CEEW report. London: Carbon Tracker.